Copy to clipboard

Copy to clipboard

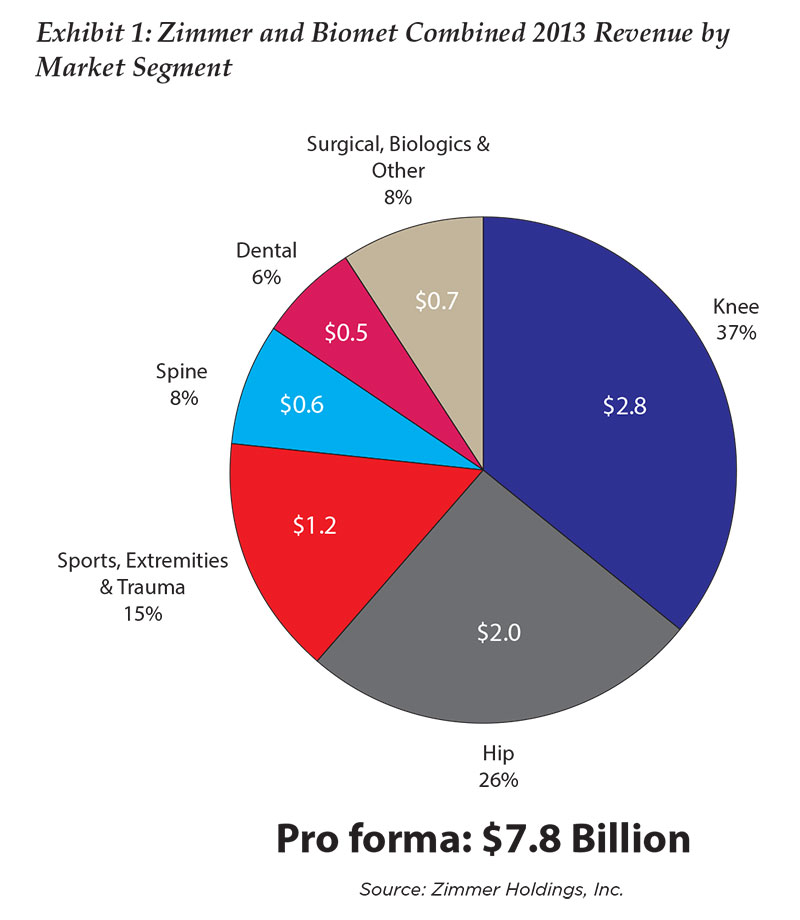

To build a more comprehensive and scalable portfolio of products, Zimmer announced its intention to acquire Biomet for $13.35 billion. With combined revenue of $7.8 billion for the calendar year 2013, the finalized deal, expected to close in 1Q15, would allow the merged company to leap Stryker and become the second largest orthopaedic manufacturer with an estimated market share of about 17 percent.

During a conference call, David Dvorak, Zimmer President and CEO, cited the company’s ability to diversify its revenue mix, create cross-selling opportunities and improve global distribution channels as benefits of the acquisition. Specifically, the acquisition gives Zimmer an edge in the knee and hip markets, as it reduces the top five competitors to four and takes the majority of the market share. The acquisition accelerates Zimmer’s growth—and market position—in the sports medicine, extremities and trauma segments by expanding its presence in emerging markets along with expanding its upper and lower joints portfolio. Finally, the purchase of Biomet would allow Zimmer to double its share of the spine market. Exhibit 1 illustrates both companies’ combined revenue breakdown by category, while Exhibit 2 shows analyst estimates of pre- and post-transaction market share for Zimmer.

Dvorak stressed that, once merged, Zimmer will have the opportunity to meet the needs of healthcare providers and patients by offering solutions throughout the entire continuum of care. For example, Zimmer’s early intervention and joint preservation technologies may be sold into Biomet’s revision portfolio.

In response to questions regarding combining product portfolios and developing pipeline activity, Dvorak said that the company will have a research and development spend of $360 million. The acquisition assists Zimmer in focusing on incremental and “game-changing” innovation while allowing the company to rapidly address current unmet needs when it comes to technologies and delivery systems.

“We need to work in closer relationships with providers, surgeons, integrated healthcare systems, whether they’re private or national in their orientation across the globe in a manner that allows us to together provide better patient outcomes and solutions, but at the same time to do that cost effectively,” he said. “This portfolio of existing products, technologies, allows us to engage in those discussions and partner in ways that we believe is going to be very comprehensive and deep and to help work together towards addressing any of the challenges that exist, whether it is a patient outcome challenge or a cost efficiency challenge.”

A principal point is that the customer—hospitals, private practices— is consolidating and will continue to do so as it faces its own pressures. “They’re going to be looking for savings as well by partnering with fewer vendors that can offer a fuller portfolio of solutions, and that’s going to be an advantage along with these integrated services,” Dvorak said.

Consolidation speaks to the larger picture of the orthopaedic industry. Reimbursement pressure, price sensitive customers, tighter FDA standards and the simple costs associated with doing business globally are expected to lead to more acquisitions amongst device makers as they seek to find savings.

Combined, Zimmer and Biomet expect synergies of $135 million in the first year and $270 million by 2017.

“With consolidation happening across the healthcare industry, management teams seem to believe bigger is better,” Mike Matson, CFA, Senior Research Analyst of Needham & Company’s Medical Technologies & Diagnostics division wrote in his analysis of the acquisition. “Bigger med tech firms have cost advantages and are able to bundle products putting smaller companies (particularly those undifferentiated technologies) at a disadvantage.”

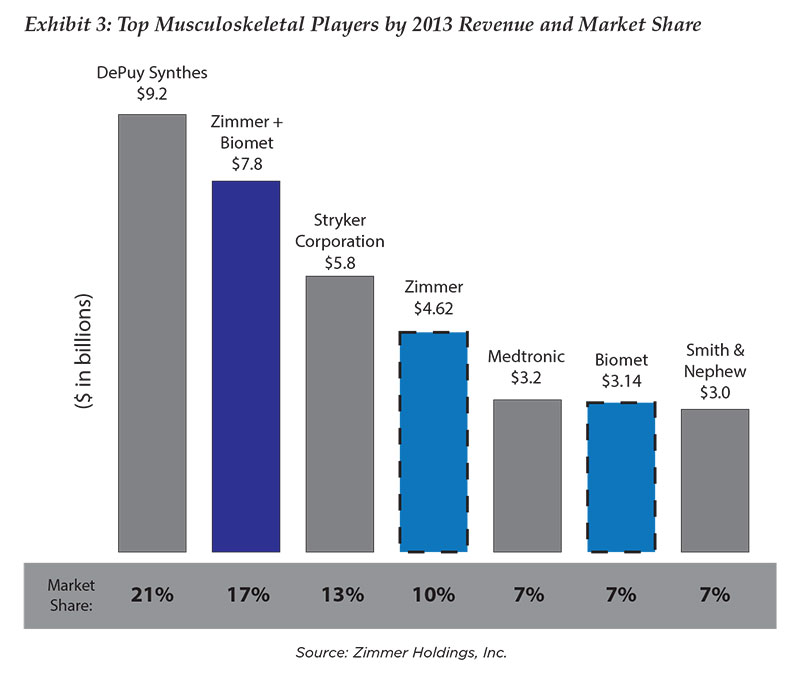

Among the industry’s larger players, Stryker and Smith & Nephew may also be negatively impacted as Zimmer surpasses them both in the ortho recon market. (See Exhibit 3.) The deal could also pressure them, and others, to get larger. Answers to many questions—effect on supply chain, employee downsizing, product elimination—will be realized in time. For now analysts have stated that, overall, the acquisition is good for Zimmer and for the industry, as device companies continue to adapt to a slowing market and a changing healthcare landscape pressured by costs, outcomes and its own consolidation.

Continue to read BONEZONE for the latest on how industry changes like this acquisition are affecting device manufacturing and the supply chain.