Copy to clipboard

Copy to clipboard

In 2009, ORTHOWORLD estimated annual global orthopaedic supplier market sales to be approximately $2 billion. At that time, slowing growth in the orthopaedic original equipment manufacturer (OEM) sector was reflected in the supplier side, though competition remained high and consolidation/collaborations continued around the globe. To this day, the orthopaedic supplier market remains highly fragmented and competitive.

On the OEM side, seven multinational OEMs – Stryker, DePuy/J&J, Zimmer, Medtronic Sofamor Danek, Synthes, Smith & Nephew and Biomet – each with $1 billion or more in annual orthopaedic device sales, currently hold the predominant share of the orthopaedic device market. The ten largest orthopaedic OEMs account for approximately 90% of the market. These leaders rely heavily upon independent suppliers for the manufacturing of implants, instruments, cases and other elements of an implant system.

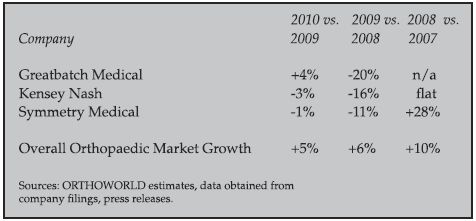

Over the past three years, growth in the supplier side of the market has “tagged along,” ebbing and flowing behind that of the OEM side. Exhibit 1 illustrates the variety in growth rates for the years 2008 to 2010, displaying orthopaedic segment growth for three publicly-traded supplier companies alongside that of the overall orthopaedic market.

Exhibit 1: Worldwide Orthopaedic Segment Sales for Select Supplier Companies, Including Overall Orthopaedic Market Growth: 2008 to 2010

Sources: ORTHOWORLD estimates, data obtained from company filings, press releases.

Despite a slowing of growth to the mid-single digits, the orthopaedic market should remain one of the healthiest among medical devices due to undeniably perfect demographics. Following is a snapshot of current market dynamics affecting both OEM and supplier sides.

OEM Market Characteristics

- ~$40 billion global market, with estimated 5% growth in 2010

- U.S., Europe and Japan account for >80% of global market with <20% of world’s population.

- The fastest growth segments are spinal, arthroscopy/soft tissue repair and trauma, with more modest growth in reconstruction implants and orthobiologics.

- The global recession has taken its toll upon the largest orthopaedic OEMs which, after years of double-digit revenue growth, posted more modest sales growth in FY10. However, growth strengthened in late FY10 and into FY11.

- Despite moderating growth, profitability has remained solid due to greater scale and commitment to operational efficiency, with recent median gross and EBITDA margins of 74% and 32%, respectively, vs. 73% and 31% from three years prior for the top 7 OEMs.

- Increased pricing pressure continues throughout the supply chain from moderating growth rates, increasing pressures from end users, Department of Justice and FDA activity.

Supplier-Specific Considerations

- Pricing pressure on OEMs is leading to pricing pressure and increased investment in automation throughout the supply chain.

- While OEMs continue to consolidate their supply chains, several also continue to divest certain manufacturing facilities.

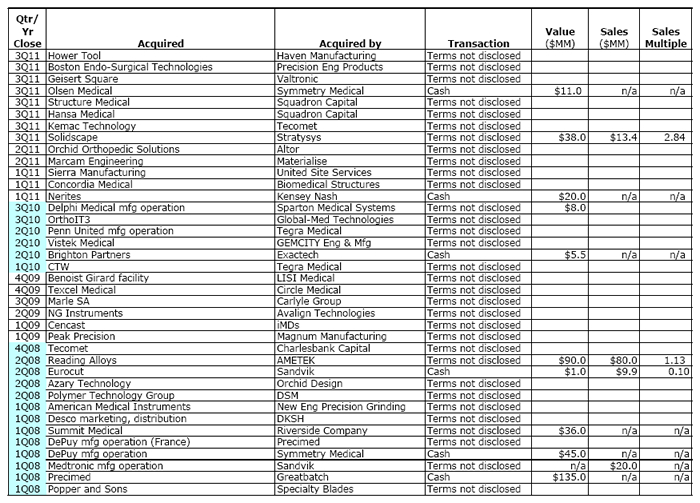

- Consolidation continues, typically entailing the merging of complementary businesses allowing suppliers to provide broader array of services to OEMs. (See Exhibit 2.)

- Entrance of industrial players into medical market, including orthopaedics.

- Continuing innovation supporting minimally invasive/computer assisted surgery, biomaterials, RFID technologies and enhanced outsourced product development.

Exhibit 2: Supplier Merger & Acquisition Activity: 2008 to 2011 To Date

Sources: Data obtained from company filings, press releases, Espicom, Capital IQ and Viant Capital LLC.

Consolidation Outlook

- Highly fragmented orthopaedic supplier market will continue to consolidate to enhance competencies, diversify client bases, expand product offerings (e.g., across implants, instruments, delivery systems), introduce other services and solutions (e.g., design services), expand geographically (local to regional, regional to national, national to international) and enhance pricing power over raw material suppliers and even up-market customers.

- Consolidation at the supplier level has also enabled providers to expand the breadth of their services specifically to differentiate the value provided to the OEMs and to spread the risk for the supplier.

- Of importance to OEMs—in addition to quality, cost and on-time delivery—is an increasing preference for larger suppliers possessing multiple capabilities which, in turn, is fueling M&A activity; a growing interest in suppliers becoming OEMs’ strategic partners; strict vendor qualifying processes (e.g., regulatory, compliance, quality, on-time delivery, lean manufacturing, speed to market, ability to innovate); a demand for financial stability with up-to-date capital investments and a broadening geographic presence.

Growth Drivers

- An aging population (world’s elderly population increasing 3x the rate of the overall population)

- A more active and longer-lived population

- An increasingly obese population

- Improved access to healthcare and improved standards of living in emerging economies (U.S. accounts for majority of global orthopaedic market, but a very minor portion of the population)

- Increased personal involvement in healthcare and consumer marketing

- Further penetration of orthopaedic procedures in less-developed nations

- Technologies, including biologics and alternative raw and bearing materials, that expand procedures to younger age groups

- Increasing prevalence of revision procedures

Evidence-based medicine, Accountable Care Organizations, physician owned distributorships, intense pricing pressure, the potential shortage of surgeons, greater data requirements for regulatory and insurance approvals, U.S. healthcare reform and the impending medical device tax are some of the major issues that will impact the orthopaedic market for the foreseeable future. Both sides of industry must accept and adapt to these new paradigms in order to gain the efficiencies required to deliver solutions to patients and surgeons, and thrive in the days ahead.

REFERENCES

Sector Bulletin: Orthopedic Supplier Market, 3Q11. Viant Capital LLC, Member FINRA.

THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®, ORTHOWORLD Inc. © 2009, 2010, 2011.

For additional information on the supplier sector, including an assessment of value of your orthopaedic business, please contact Viant Capital (Member FINRA) at www.viantgroup.com or 415.820.6100. Click to access the author’s emails: David Reilly and Jean-Paul Burtin.