Copy to clipboard

Copy to clipboard

The orthopaedic contract manufacturer market comprises hundreds of companies that serve orthopaedic device manufacturers and, in many cases, other contract manufacturers. We estimate that revenue for this market reached $5 billion in 2017, +7.6% or $360 million from 2016, as published in THE ORTHOPAEDIC INDUSTRY ANNUAL REPORT®.

The medical device contract manufacturing space is primed for growth due to outsourced production by the industry’s largest device companies, as well as orthopaedic startups that largely outsource their manufacturing.

One sign that this segment is well-positioned is the number of private equity firms that have invested in contract manufacturers with the expectations of performance improvements and sizeable returns.

In this article we’ll look at the sector’s market forces, capability trends, main players and future growth drivers to provide you with a greater understanding of how your supplier partners are transforming their businesses.

Market Forces

The contract manufacturer space is shaped by four primary market forces that have been in play for the better part of the last decade: price pressure, supplier reduction, merger & acquisition and labor shortages.

- Price Pressure: Device companies, squeezed on implant price by their hospital customers, are passing those demands of lower cost on to their supplier partners. The majority of market circumstances impacting contract manufacturers correlate to this intensified focus on price.

- Supplier Reduction: In an effort to contain costs and maintain quality, device companies have decreased the number of suppliers they’ll use for specific work, from prototyping to manufacturing of instruments and implants. For device companies, this mandate sets internal expectations for all departments and provides purchasing departments leverage with contract manufacturers. Tier-one contract manufacturers must maintain their status on device companies’ preferred vendor lists through competitive prices, consistent quality and on-time delivery.

- Mergers & Acquisitions: The uptick in M&A activity throughout the supply chain has been a large and sometimes unpredictable disruption to contract manufacturers of all sizes. When mega mergers occur on the device company side, like DePuy + Synthes and Zimmer + Biomet, manufacturing is often halted; uncertainty arises for contract manufacturers while companies determine which products will remain in their portfolios. In addition to M&A of customers, contract manufacturers must remain aware of transactions taking place amongst their own supplier partners. Larger contract manufacturers often outsource portions of the manufacturing process to smaller companies. As tier two and three manufacturers find it increasingly difficult to compete, they seek to be purchased or to divest their orthopaedic businesses. Thus, in today’s market, all manufacturers are looking for and validating new manufacturing partners.

- Machinists: Hiring, training and retaining machinists remains an industry-wide challenge. Lead times, especially on the instrument side, have been a consistent response to questions posed to suppliers about their greatest challenge this year. A lean candidate pool has made it difficult for companies to increase manufacturing volume, reduce lead times and meet deadlines. It’s largely recognized across the industry that investments in automated processes and tools are needed to offset the people problems.

These four market forces are expected to remain for the foreseeable future, influencing contract manufacturers’ decisions on ways to maintain market share and profitability. This includes deeper consideration of their current capabilities and services.

Capability Trends

Traditional manufacturing competencies—forging, grinding, laser marking, milling, molding, turning, etc.—continue to meet the core needs of device manufacturers. However, in response to device companies’ requests and to remain competitive, contract manufacturers have added services to their portfolios. Diversification has taken place throughout the manufacturing process—regulatory and design, packaging and logistics. The idea is that if contract manufacturers are able to provide greater value to their device company customers, they may not face as much stiffness on price while adding new revenue streams.

Trends in device company product introductions have led us to believe that emergent manufacturing approaches like additive, coatings and materials, as well as niche markets like single-use instruments or inventory management tracking, will be attractive investments for some suppliers.

Additionally, large contract manufacturers have launched R&D or innovation centers to explore product ideas and manufacturing techniques to then apply to their customers’ products. Dedicated suppliers like materials companies and equipment manufacturers have followed this model in recent years.

Players

Revenues for this space are significantly more difficult to estimate than for the device company space as the majority of companies are privately owned, derive portions of their revenue from customers outside of orthopaedics and are also consolidating. In finalizing our numbers, we asked contract manufacturers and reputable industry contacts for validation. As was previously noted, we estimated that this portion of the market surpassed $5 billion in 2017. We expect this segment of the market to grow in the 7% range annually for the next five years.

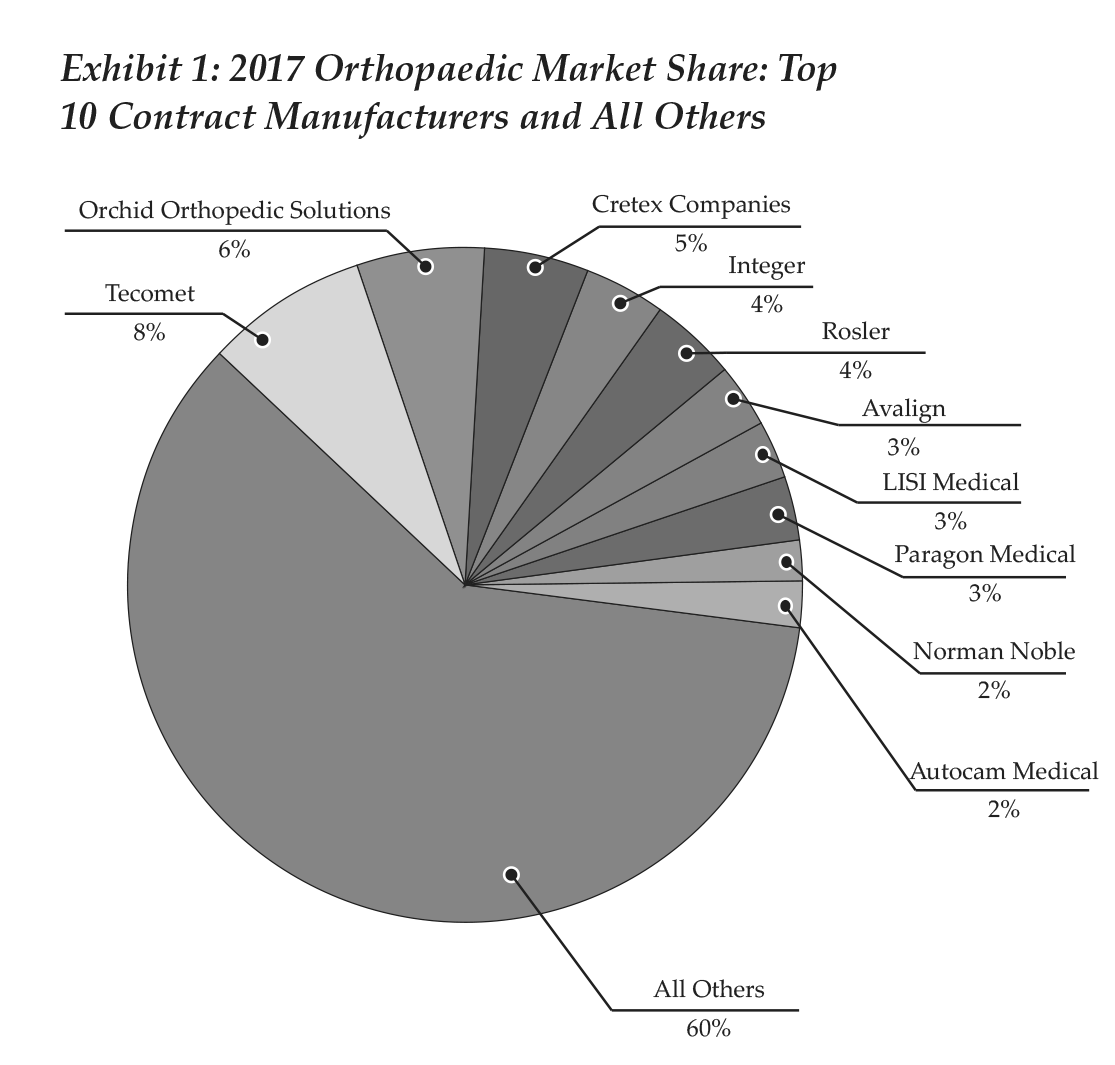

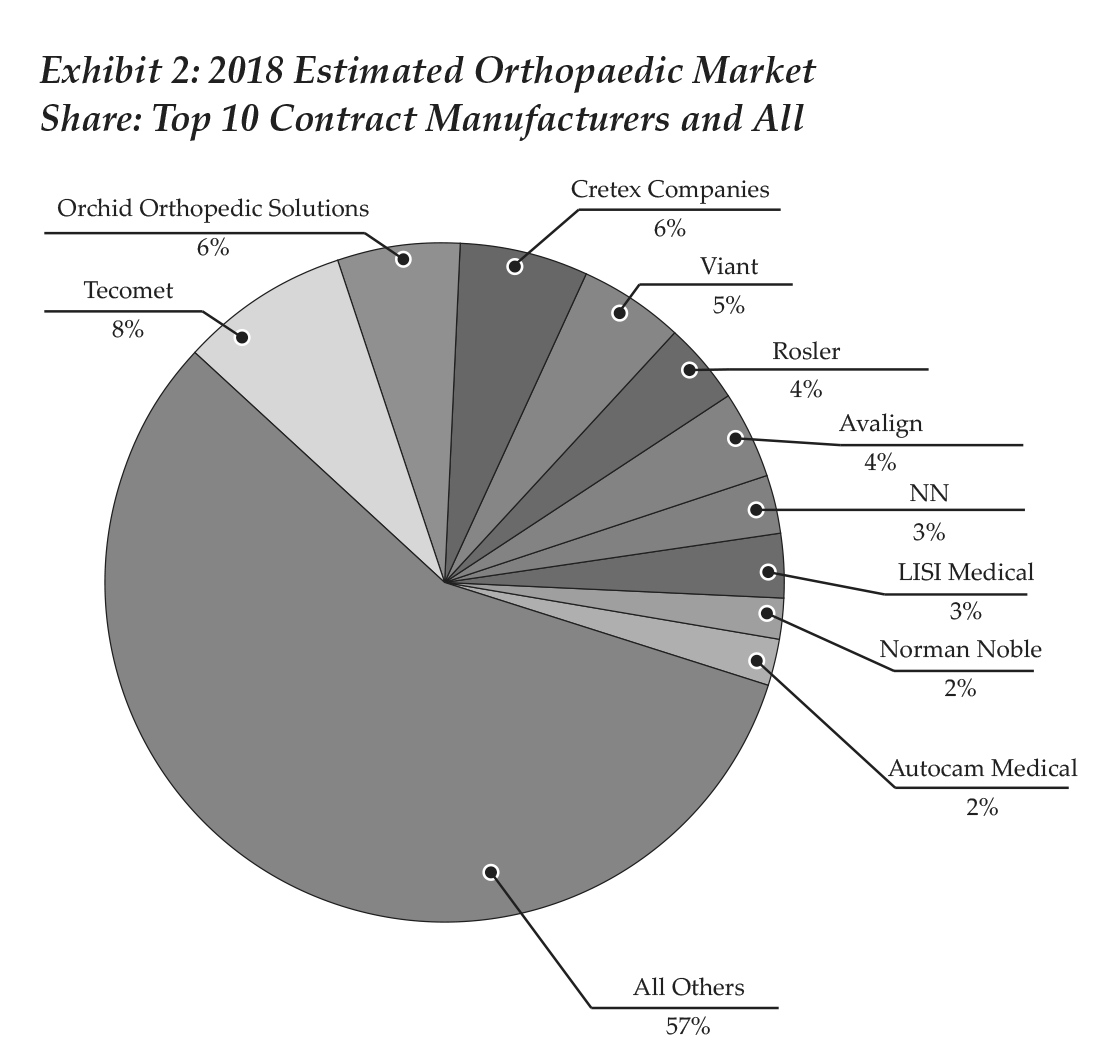

By our figures, 10 contract manufacturers (Tecomet, Orchid Orthopedic Solutions, Cretex, Integer, Rosler, Avalign, LISI Medical, Paragon Medical, Norman Noble, Autocam Medical) generated orthopaedic revenue above $100 million in 2017, and combined accounted for 40% of the segment’s revenue. These companies and their ranking are illustrated in Exhibit 1. As can be seen in Exhibit 2, recent M&A activity changed the names that appear in the pie, as well as the positions of some players.

In 2018, Integer was acquired by MedPlast, which then rebranded as Viant. MedPlast was the parent company of OrthoPlastics and had in the last two years purchased other businesses, such as Coastal Life Technologies and Vention Medical’s Device Manufacturing Services. Viant caters to a diverse group of medical device specialties, with capabilities that include design to material expertise, manufacturing, packaging and supply chain management.

NN also joined the top ranking with its purchase of Paragon Medical in 1H18. NN, a public company, stated that it expects its Life Sciences business to reach revenue between $275 and $300 million in 2018; of that, about 50% to 60% will derive from orthopaedics. In total, we predict that the 10 largest contract manufacturers will end 2018 with a combined 43% market share.

Closing Comments

Contract manufacturers of all sizes are engaged in acquisitions and expansion of capabilities, facilities and markets in response to their customers’ requests. Ultimately, contract and device manufacturers seek greater continuity between their business processes to solidify plans that lower cost and increase efficiency, resulting in higher margins for both entities. Contract manufacturers that are able to engage customers in these conversations will be better positioned to respond with manufacturing and technical support.

Movements that will define the contract manufacturer space in the next five years are as follows:

- M&A activity will continue, as tier-one manufacturers seek to remain competitive with other tier-one manufacturers, as well as with suppliers and service providers. This means that manufacturers will purchase companies with a strong regional presence (U.S., Europe, Asia, etc.) and companies with strong competencies outside of traditional manufacturing (coatings, design, regulatory, packaging). These investments will be financed in part by private equity firms that have recently entered or will enter the space, and will be assisted by tier-two and tier-three suppliers attentive to market dynamics and well-positioned to be purchased.

- Contract manufacturers will continue to invest in facility expansions and new offices globally to more efficiently and effectively serve their customers.

- Contract manufacturers able to retain machinists or automate more of their plant floors will be better situated to handle the vast fluctuations in customer orders.

- Device companies will continue to look to partners for assistance with more complex manufacturing processes, particularly for products in growing areas of minimally invasive surgery like spine and trauma.

- With larger device companies experiencing slower growth and their own set of unique challenges, contract manufacturers will seek business from a mix of the top 10 device companies, faster-growing next-tier players and startups.

Considering these factors, we expect that the contract manufacturer market will grow in the high single digits over the next five years and surpass $7 billion by 2022.