Copy to clipboard

Copy to clipboard

I cannot recall a more unsettling year in the more than 20 years that I’ve been involved in orthopaedics. Last year, 2009, began with a global economic meltdown and ended with many folks still scared into non-action. Fear and uncertainty reverberated down the halls of many a hospital and in the conference rooms of many an orthopaedic manufacturer. Patients postponed surgeries, admissions fell and hospitals tightened their belts. Some even cancelled surgeries due to budget constraints. Insurers questioned the necessity of procedures and more frequently deemed tried and true technologies to be “experimental.” FDA turned away more than one promising technology, resulting in failed businesses and damaged revenue streams.

And it all rolled downhill and settled at the doorstep of the orthopaedic manufacturer (and its supplier). In the end, our industry was better off than some and worse off than others.

The year marks the first in my memory of orthopaedic companies posting sales declines. Three large players in the arthroscopy segment showed decreases due to hospitals curtailing capital equipment purchases. Hip and knee sales for a few key players dropped as well, and suppliers felt the brunt, with two of the largest orthopaedic suppliers posting sales decreases of more than 20 percent, largely due to their bigger customers working down inventory.

Within orthopaedics, 2009 was characterized as one of intense price pressure in most segments of the market. An increased use of tenders outside the U.S. served to cap prices for many orthopaedic products. Zimmer repeatedly noted negative price, while DePuy reported slight declines in price throughout the year. Price was flat overall for Stryker for much of the year with Biomet witnessing neutral pricing for joint replacement in the U.S. and some slightly negative prices outside the U.S.

We had initially thought that the trauma market would be fairly well insulated from economic moodiness around the world. Wrong we were. The segment’s growth did decline. More than one manufacturer attributed the decrease in market growth to less construction and fewer people travelling by car. In addition, less discretionary income left more people at home and not on the ski slopes (or other sports venues), where they would have incurred certain kinds of fractures.

Spine companies, too, felt some intense price pressure, although not as much pushback on procedures as in joint replacement. A typically younger and working age patient was more likely to seek surgery to ensure a return to work (and a living). At the same time, more than one manufacturer faced reimbursement challenges for technologies and procedures that have been in use with good results for a number of years.

Hardest hit of all market segments in 2009 was that for capital equipment products like arthroscopes, cameras, etc., which are an integral part of many hospital operating rooms. Three of the arthroscopy market’s leading companies – ConMed, Smith & Nephew and Stryker – posted negative growth in capital equipment product sales off and on throughout the year, and these are businesses that two years ago were growing in excess of ten percent (nearly 20 percent for Stryker!).

On the bright side, the curtailing of spending on big ticket items by hospitals started to relax in the second half of 2009, in the U.S. at least. (Europe lags behind in recovery.) Several joint replacement companies noted more patients coming in for surgeries, and a colder winter may contribute to an increase in falls, which would help to renew some vigor in the trauma segment.

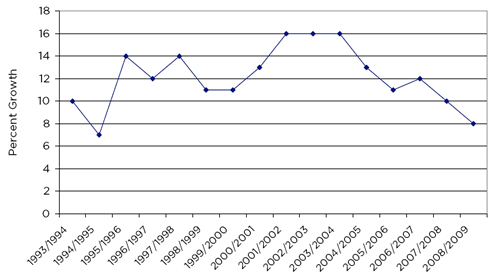

At press time (mid-February), 11 publicly-traded companies had reported their 2009 results, including five of the largest joint replacement entities and Synthes, the market leader in trauma. With these companies’ results in hand, we’re projecting a 2009 global orthopaedic market value at more than $38 billion, for an increase of between six and eight percent over 2008, the first single-digit market growth since the mid-1990s, as Exhibit 1 illustrates.

Exhibit 1: Orthopaedic Market Growth 1993 to 2009

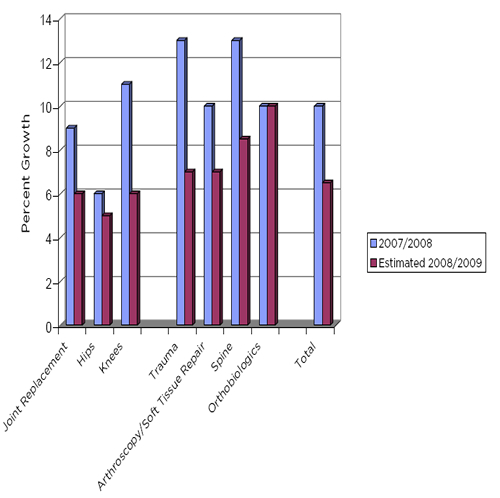

Exhibit 2 compares growth for market segments for the last two years.

Exhibit 2: Market Growth 2007 to 2009E

Stability and cautious optimism marked 2009. For 2010, we hope for an improvement in the economic environment globally and some resolution to the madness surrounding healthcare reform in the U.S., preferably without a tax on medical device companies.

Stability and cautious optimism marked 2009. For 2010, we hope for an improvement in the economic environment globally and some resolution to the madness surrounding healthcare reform in the U.S., preferably without a tax on medical device companies.

Into 2010, we expect a rebound in capital equipment sales, but not to pre-2009 levels.

We don’t expect to see a big bolus of joint replacement or spine business due to pent up demand. Companies expect price pressures to continue in joint replacement, trauma and spine, with average selling prices settling in at flat to slightly negative. At the same time, we’ll likely see an uptick in the contribution of mix due to introduction and/or further penetration of products like cups and nails from Zimmer, Synthes’ Angular Stable Locking and Vertebral Body Stent Systems, fracture repair plates and shoulder from Biomet, Exactech’s shoulder, knee and spine products, Stryker’s new Rejuvenate modular hip system, etc. Also look for companies to more frequently use “superior” clinical results as a means to derive premium prices for new products and/or win new business.

All told, 2010 will probably settle in at growth in most segments in upper single digit levels, with spine and biologics outpacing others by a point or two, as has been the case for years. It ain’t great, but again it’s better than some and worse than others. And at least we’re not building bombs.

Shirley A. Engelhardt is President and Founder of ORTHOWORLD Inc. and a founding partner of Knowledge Ventures, LLC, a venture capital firm solely focused on orthopaedic investments. Mrs. Engelhardt is the world’s foremost authority on the global orthopaedic markets and has authored thousands of articles on current and emerging trends, market dynamics and factors affecting the markets. She has accurately predicted nearly every major market trend of the past decade, while developing an international client base of hundreds of public and private entities.

Prior to founding ORTHOWORLD, Mrs. Engelhardt was Director of Market Research and Strategic Services for DePuy and Director of Marketing for the technology transfer arm of Case Western University. She holds a Bachelor of Arts degree in French from Virginia Polytechnic Institute and State University and an MBA from The Louisiana Tech School of Management.