Copy to clipboard

Copy to clipboard

Although a majority of the work performed by manufacturers involves producing products for customers, a significant amount of work is also performed after their products are produced and before they are shipped to the customer. Understanding the impact of “fulfillment costs” is critical to a company trying to understand customer profitability. However, these two cost categories—manufacturing and fulfillment—do not represent all of the costs that must be understood to accurately measure the profitability of customers. Many costs that separate desirable customers—those whose behavior keeps support costs to a minimum and enhances company profitability—from the less-desirable ones—those whose behavior increases costs and decreases profit—lie hidden in that great “blob” of costs christened by most organizations as “selling, general and administration” or simply SG&A.

Let us consider the case of one manufacturer/distributor that has carefully measured its manufacturing and fulfillment costs and arrived at the customer profitability analysis shown in Exhibit 1.

Exhibit 1: Profitability by Customer

Based on the cost of both manufacturing their products and fulfilling their customers’ orders, all five customers appear to generate the same level of profitability.

There remains, however, that $3 million “blob” of SG&A costs that are spread evenly among the five customers as a flat 20 percent of product and fulfillment costs. Does this flat rate provide for a fair assignment of these costs based on the amount of work required by each customer of the activities included in SG&A? Is the work performed by sales and marketing the same for each customer? How about the amount of customer service or cost estimating and quoting? Perhaps a closer look at the various activities incorporated into SG&A—activities usually considered “just the cost of doing business”—is warranted.

The manufacturer/distributor evaluated the various activities comprising SG&A and determined that 100 percent of sales and marketing, production control, customer service and cost estimating/quoting and portions of accounting and quality control are actually “driven” by customer behavior; they are not general “cost of doing business” at all. These customer driven-costs represent half of the $3 million included in SG&A and are detailed in Exhibit 2.

Exhibit 2: “Non-General” SG&A Costs

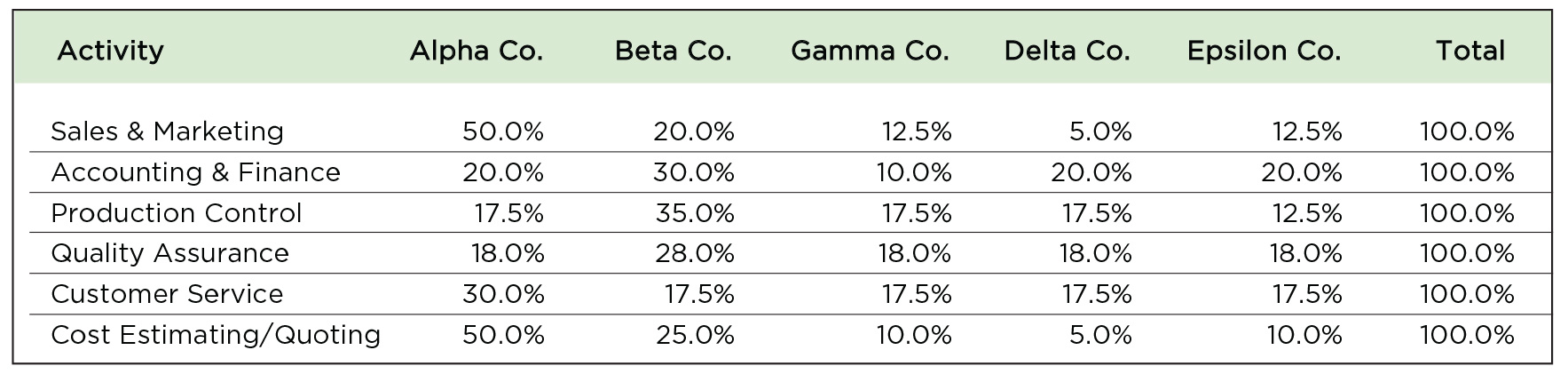

While exploring how each of these activities relates to its individual customers, the company noted the following:

Sales & Marketing

Almost half of the company’s sales and marketing effort relates to Alpha Co., the largest organization it serves. Alpha shops its business around to a multitude of vendors, requires an inordinate number of meetings, changes its mind regularly and requires scores of special reports and updates. In addition, the company’s “hit rate” on quotes to Alpha is extremely low. Delta Co., on the other hand, requires very little attention. It asks the company to quote on work, awards it with a high percentage of the jobs it quotes and requires very little attention between the times a job is awarded and when production/distribution begins. The other customers require about the same amount of attention, although Beta Co. demands slightly more than the others.

Accounting & Finance

The customer-related accounting and finance activities relate primarily to billings and collections. Getting money out of Beta Co. is often like pulling teeth, while Gamma Co. pays on a timely basis without fail. The other customers occasionally cause a collection problem, but those instances are few and far between.

Production Control

In addition to causing collection problems, Beta Co. also can’t seem to forecast its demand with any kind of consistency. As a result, production control is constantly changing production schedules to accommodate Beta Co.’s ever changing demand. Epsilon Co. never changes its schedule once the order is received, while the other customers do make changes, but they are infrequent.

Quality Assurance

The quality documentation required by Beta Co. is far greater than that required from any of the company’s other customers. Special pre-production and post-production reports abound. Quality documentation for all other customer’s business, on the other hand, is easily met by the company’s standard quality practices.

Customer Service

The same factors that cause Alpha Co. to demand an inordinate amount of attention from sales and marketing result in it requiring almost a third of the work performed by customer service. Numerous customer visits, regular order inquiries and status reports are all part of dealing with this large organization. None of the other customers demand such attention.

Cost Estimating/Quoting

The large number of quotations required, their complex nature and the low “hit rate” on Alpha Co.’s business also puts a huge demand on cost estimating/quoting requiring, as was the case with sales and marketing, almost half of its work. Beta Co.’s quotation process is also more complex and its “hit rate” lower than the other customers, but not nearly as bad as Alpha’s. Delta Co.’s quotes, on the other hand, are simple and the “hit rate” high, requiring a fairly low amount of work from cost estimating/quoting.

The demand of the five customers for these six support activities expressed in percentages is summarized in Exhibit 3.

Exhibit 3: Activity Demand by Customer

Applying these percentages to the cost of the six support activities results in the cost distribution and “Customer Support Rates” shown in Exhibit 4.

Exhibit 4: Support Activity Cost Distribution and Customer Support Rates

Finally, applying these Customer Support Rates to the business generated by each of the customers results in the revised view of customer profitability shown in Exhibit 5.

Exhibit 5: Revised Customer Profitability

As can be seen in Exhibit 5, all customers are still profitable, but they are not all equally profitable as shown in Exhibit 1. Gamma, Delta and Epsilon all prove themselves to be “desirables” with behavior that results in profits greater than the 10 percent average, while Alpha’s and Beta’s behavior place them in the “less-desirable” category whose excess costs drive their profit below the 10 percent average.

The primary purpose of cost information at a manufacturer/distributor is to provide insights that will help the company’s management make decisions that enhance profitability. (Sorry, financial accountants, valuing inventory and calculating cost of goods sold is a secondary purpose—making money is inherently more important than counting it.) This fact raises an important question: How does this knowledge of customer support cost make the company more profitable? After all, the customer isn’t going to allow us to increase prices; they’d just buy the product from someone else. We’re probably not going to drop the customer; its volume is important as it “absorbs” a lot of the cost we wouldn’t be able to eliminate if its business went away.

As noted in my earlier article on fulfillment costs, knowledge is power and what gets measured gets done. Measuring the work required to support each customer—or in many cases, each category of customer—enables an organization to: 1) work with customers to modify the behavior that creates the excess support costs (possibly using price reductions that share the savings as an incentive), 2) understand that the customer is what they are and modify the company’s own systems to more effectively handle the customer’s “less-desirable” behavior, and 3) better manage marketing efforts to attract those types of customers that generate more profitable work. All such information is actionable and can help a company improve profitability. It is not just created to provide greater insight into the past; it’s provided to lead the way into a more profitable future.

During more than 25 years as a consultant, Doug Hicks has championed the development of practical, down-to-earth cost management solutions for small and mid-sized organizations. In that time, he has helped nearly 200 organizations transform their history-oriented accounting data into customized, value-enhancing decision support information that provides accurate and relevant intelligence needed to thrive and grow in a competitive world. He shares his experience through seminars conducted throughout the U.S., in trade and professional periodicals and two books, including I May Be Wrong, But I Doubt It: How Accounting Information Undermines Profitability.